Multi Asset Markets Recap: Week of 11 May 2026

The unresolved US–Iran war kept Hormuz effectively constrained all week, with tanker attacks continuing and the Trump–Xi Beijing summit delivering only vague in principle rhetoric rather than concrete pressure on Tehran. US April CPI hit 3.8% year-on-year, the highest since May 2023, with ~40% of the monthly gain driven by energy. Equities surged to records mid-week before a sharp Friday reversal. Kevin Warsh’s narrow confirmation as Fed chair, combined with hawkish Fed commentary, fully repriced markets toward at least one hike by early 2027, while the US 10-year yield broke above 4.59%, though corporate credit spreads stayed tight. The dollar strengthened, Bitcoin fell below $79,000, and gold and silver nearly erased monthly gains as real yields dominated safe-haven flows.

Macro and (Geo)Politics

Across the week, markets were dominated by the unresolved US–Iran war and its impact on oil flows through the Strait of Hormuz. Iran’s proposal for a gradual reopening was rejected by Washington as totally unacceptable, and the week saw further tanker attacks and seizures, leaving Hormuz effectively constrained and embedding a persistent war premium in crude.

The Trump–Xi summit in Beijing was treated as an informal deadline for progress on both the Iran conflict and US–China trade tensions. Hopes initially rose as China signalled support for a diplomatic resolution and the two sides discussed limited tariff cuts and a more managed trade framework, but the summit ultimately delivered only warm rhetoric and an in principle agreement with no concrete commitment from Beijing to pressure Tehran, disappointing markets looking for clearer de‑escalation.

In Europe, UK politics remained an overhang to the country, as Labour’s heavy local‑election losses led to calls for Prime Minister Keir Starmer to quit, and later in the week reports emerged that Health Secretary Wes Streeting was preparing a leadership challenge, contributing to modest sterling softness.

On the macro data front, US April CPI accelerated to 3.8% year‑on‑year, the highest since May 2023, with roughly 40% of the monthly gain driven by higher energy costs linked to the Iran war. Core CPI also surprised to the upside at 2.8% year‑on‑year, while 3.6% wage growth left real pay slightly negative.

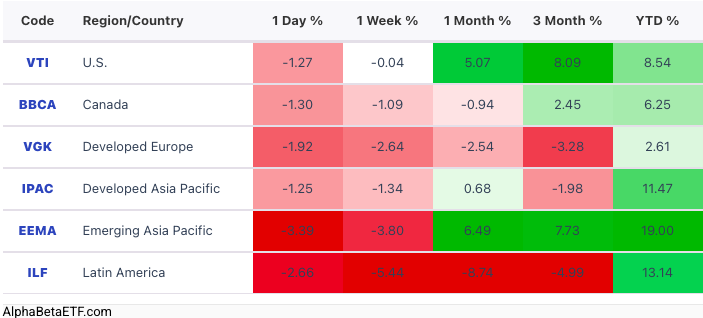

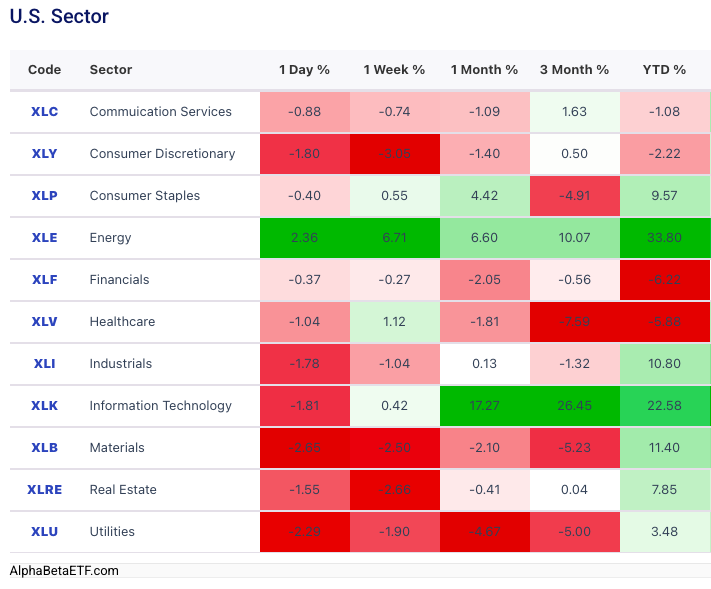

Equity

Equities started the week strongly and ended it with a pullback. The S&P 500 extended winning streak to new records on Thursday but reversed on Friday. Europe, Asia and Emerging Markets all saw a larger degree of correction over the week. Semiconductor (SOXX) and AI leaders (BAI) were volatile, with South Korea (EWY) hit particularly hard after a presidential policy chief floated the idea of a “citizen dividend” funded by taxes on AI profits. The segment rebounded as Cisco raised sales guidance and flagged strong AI‑networking and security demand, and Ford rallied on launching a unit to supply power solutions to data centers. Yet, sentiment dragged the group on Friday as the Iran situation intensified despite Nvidia’s news that it could sell H200 chips into China.

While mega‑cap growth and AI leaders powered index‑level records mid‑week, the late‑week risk‑off move was broad. Small caps (IJR) underperformed significantly, signalling that selling pressure extended well beyond the largest names and marking a rotation toward lower‑beta, higher‑quality parts of the market.

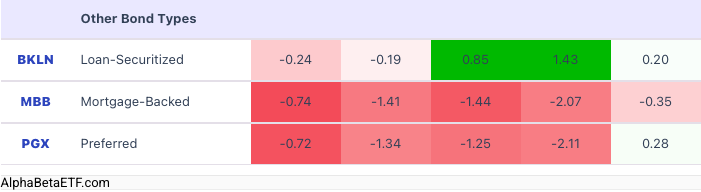

Fixed Income

Global sovereign yields marched higher as inflation surprises and geopolitics repriced the policy path. US 10-year Treasury yield went above the critical 4.5% level to 4.59% on the back of hot CPI data and a surge in oil price again.The confirmation of Kevin Warsh as Fed chair by the narrowest margin on record and hawkish commentary from officials such as Kashkari and Collins caused Fed funds futures to move from tentative cut pricing to higher‑for‑longer.

Markets were almost fully pricing at least one 25bps hike by early 2027 rather than cuts in 2026. Ultra‑short‑term TIPS (RBIL) stood out as one of the few fixed‑income ETF segments that avoided a sell‑off. US corporate spreads remained tight though, indicating that most of the pain so far has come via higher risk‑free rates rather than a sudden repricing of credit risk.

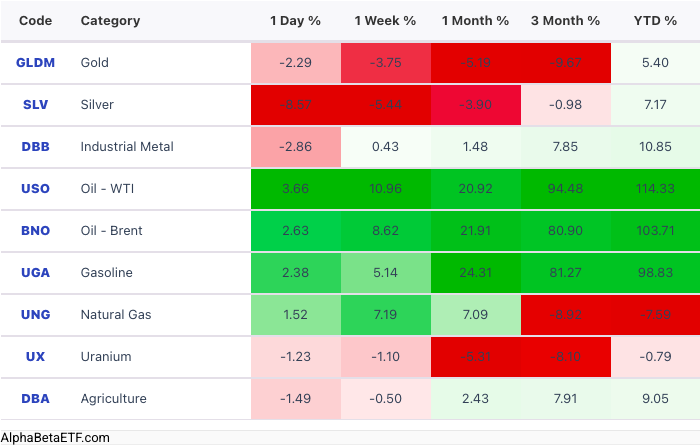

Commodity

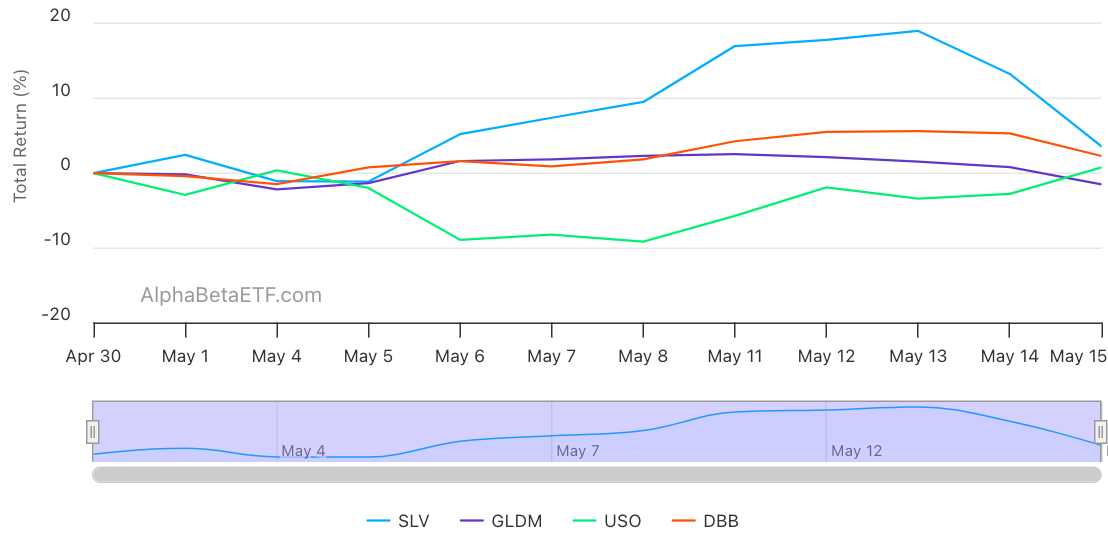

Oil (USO) remained the central macro swing factor throughout, as stalled reopening efforts and new shipping attacks rekindled fears of sustained supply disruption, and a larger‑than‑expected US crude inventory draw reinforced the story of tightening physical balances despite demand concerns. Gold (GLDM) eased slightly even as geopolitical news worsened, struggled to rally despite upside inflation surprises, then weakened further as higher real yields and a stronger dollar eroded its appeal. Gold had breached below $4,550 and silver (SLV) had corrected sharply to below $76, almost unwinding month‑to‑date gains. The Indian government responded to the twin pressures of rising oil and FX‑reserve concerns by tightening duty‑free gold‑import rules and raising gold and silver import tariffs sharply.

Currency

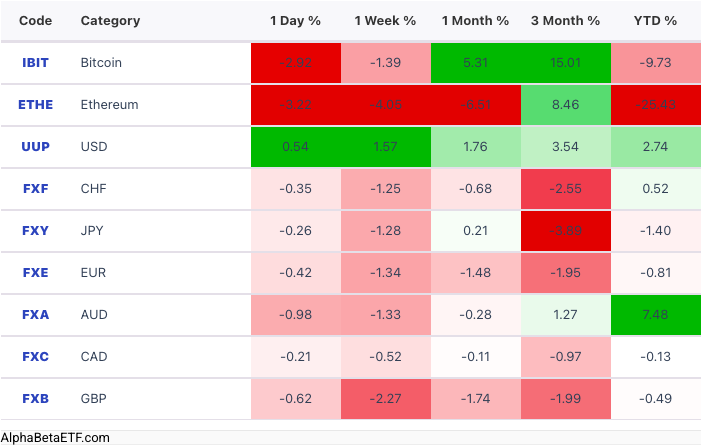

Crypto currencies corrected alongside broader risk assets, with bitcoin (IBIT) drifting down toward $78,000, leaving it below its recent $79,000–82,000 range. The dollar strengthened over the week as inflation shocks, higher yields and geopolitics combined. In the UK, ongoing talk of a potential leadership challenge to Prime Minister Starmer added an extra drag to sterling. Higher crude prices, elevated global yields and ongoing Middle East tensions were undermining the yen, with USD/JPY trading well above 158 and reversing much of the benefit from suspected FX interventions, and keeping Emerging Markets currencies under pressure.

The Week Ahead

US: FOMC minutes, Initial jobless claims, May Preliminary PMI

Europe: April CPI

Japan: Q1 GDP