Multi Asset Markets Recap: Week of 18 May 2026

Macro and (Geo)Politics

Across the week, markets were dominated by the unresolved Middle East conflict and the repeated swings in diplomacy around Iran, which kept the Strait of Hormuz effectively constrained, and no concrete breakthrough on the nuclear programme was achieved. President Trump indicated on Saturday that a deal with Iran is nearly complete and will be made public soon. He noted the agreement involves reopening the Strait of Hormuz but offered no additional specifics at this time.

The most important macro read was the U.S. preliminary May PMI, which showed a clear split between manufacturing and services. The composite PMI came in at 51.7, with manufacturing jumping to 55.3, a four-year high and well above consensus, while services stayed only barely in expansion territory at 50.9. Prices charged accelerated, suggesting the economy was seeing stockpiling ahead of higher costs, but also building inflationary pressure beneath the surface.

U.S. Composite PMI:

Outside the U.S., the U.K. labour market softened enough to give the Bank of England some relief, with median wage settlements easing to 3.0% from 3.4% in the three months to April and unemployment rising to around 5% in the three months to March. U.K.’s data was echoed in the euro area, where flash May PMI fell to 47.5, well below expectations, highlighting a much weaker growth backdrop than the U.S.

Eurozone Composite PMI:

Emerging markets also moved into the spotlight. Brazil Finance Ministry raised the 2026 inflation forecast to 4.5% from 3.7%, explicitly citing the oil shock from the Middle East conflict and implying a shallower rate-cut path ahead. Bank Indonesia surprised markets with its first rate hike in two years, raising the 7‑day reverse repo rate by 50 bps to 5.25% (vs 25 bps expected) to stem heavy rupiah weakness and pre‑empt imported inflation from higher oil prices. These developments reinforced the idea that some EM central banks still need to tighten into this environment.

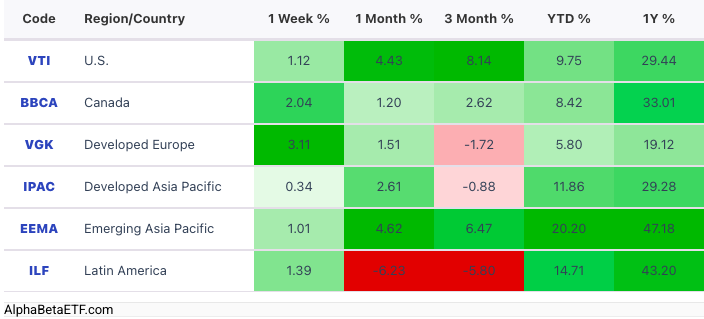

Equity

Despite weak Eurozone PMI data, Developed Europe (VGK) was the major region with best return over the week, thanks to easing geopolitical tensions.

As more investors focus on SpaceX’s IPO, related thematic ETFs like Procure Space ETF (UFO) are under the radar again. Utilities (XLU) was driven by the deal where NextEra Energy agreed to acquire Dominion Energy, the largest power‑sector transaction in history. The deal shall create what is expected to be the world’s largest regulated electric utility and give NextEra control of Dominion’s high‑growth Virginia data center alley, a focal point for AI‑related electricity demand. Retail (XRT) was another standout sector, as off-price retailers TJX Companies and Ross Stores surged after reporting strong earnings and comparable store sales growth, and raised 2026 guidance.

Growth (IVW) was sold off mid-week as long-term treasury yields spiked up, hurting valuation of growth stocks, and failed to recover even though 10-year Treasury yield fell later in the week, as yields remain elevated.

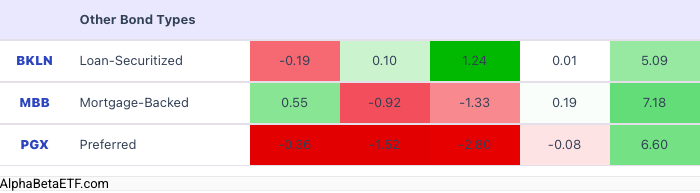

Fixed Income

The fixed-income market was driven by the same oil and inflation narrative that shaped equities. Long-dated sovereign yields pushed higher globally in the middle of the week as investors demanded more compensation for inflation and fiscal risk. However, later in the week, the market repriced lower as geopolitical concerns eased and inflation fears cooled, sending the U.S. 10-year Treasury yield eventually down week-over-week.

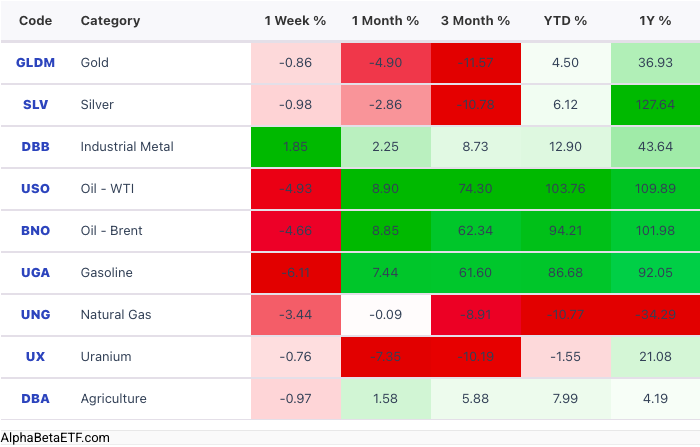

Commodity

Oil (USO) was the week’s dominant commodity, surging early on Gulf supply fears and then whipsawing lower as diplomacy improved and markets priced in a better chance of a phased U.S.–Iran deal. Gold (GLDM) moved more cautiously after the sell-off last week. JP Morgan lowered its 2026 average gold forecast to 5,243 dollars per ounce from 5,708 dollars, citing weak near-term investor interest, but still expects prices to trend toward 6,000 dollars by year-end as macro uncertainty persists. Industrial metals (DBB) and Copper (CPER) received some support from positive AI sentiment.

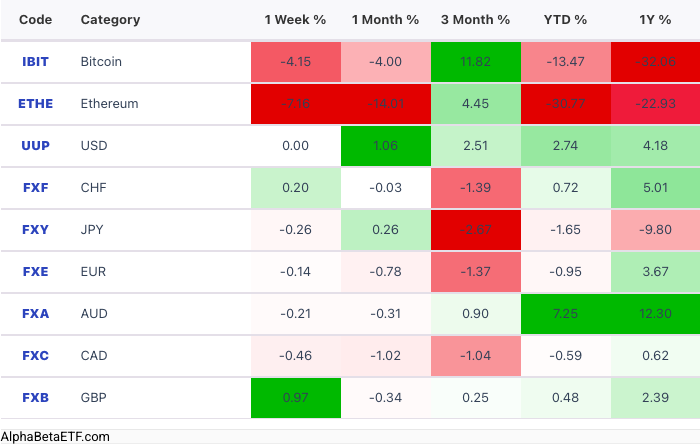

Currency

Bitcoin (IBIT) continued its weak trend with a 4% decline. U.S. Dollar (UUP) was flat, while plenty of other major currencies dropped modestly. GBP (FXB) gained as larger-than-expected slowdown in wage growth and easing U.K. labor data caused investors to adjust expectations regarding when and how much the Bank of England will cut rates this year.

The Week Ahead

US: Q1 GDP, April PCE (Personal Consumption Expenditures)

Earnings: Technology – Salesforce, Dell, Synopsys