Multi Asset Markets Recap: Week of 25 May 2026

Macro and (Geo)Politics

On the U.S.–Iran negotiation process, media reports said U.S. and Iranian negotiators had agreed to a 60-day memorandum of understanding to extend the ceasefire and reopen the Strait of Hormuz within about a month, in exchange for restrictions on Iranian uranium and progress on frozen assets, though the deal still required President Trump’s sign-off and faced resistance from Iran’s Supreme Leader.

U.S. saw downward revision to Q1 2026 real GDP growth to an annualized 1.6% from 2.0%, driven by weaker inventories and softer consumer spending. At the same time, April PCE inflation rose 0.4% month-on-month and 3.8% year-on-year, with core PCE at 3.3%, the highest annual reading since May 2023. That combination reinforced a soft growth with sticky inflation backdrop and raised concern about a stagflation-style policy dilemma for the Fed.

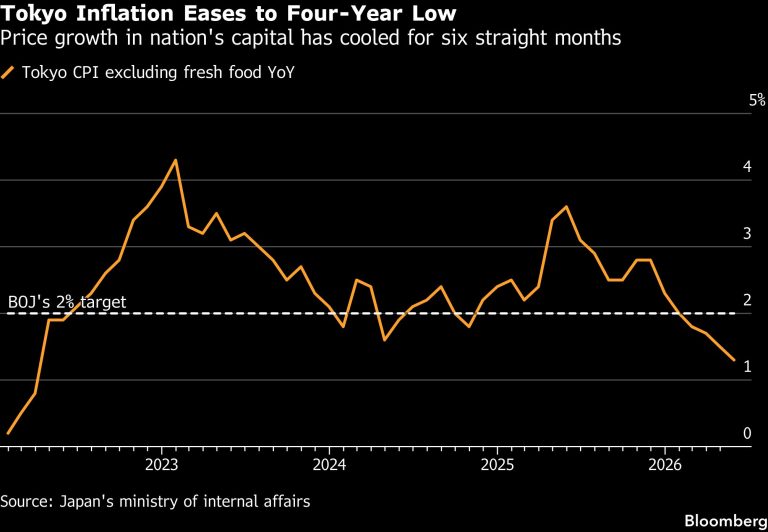

Outside the U.S., New Zealand held the Offiial Cash Rate at 2.25% and kept a tightening bias, saying more rate increases would likely be needed this year. Japan’s Tokyo inflation cooled, but service prices stayed firm enough to keep BOJ hike expectations alive, especially with the yen approaching the critical 160 level. The broad message across major economies was that growth was softening, but inflation pressures from energy and exchange rates were still far from fully contained.

Equity

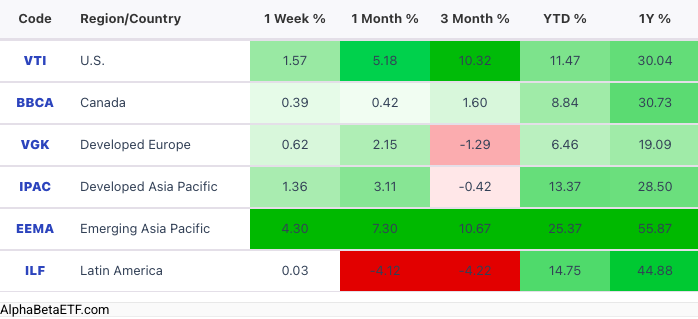

U.S. equities were led by A.I.-linked technology, which also drove the strong performance in South Korea (EWY) and Taiwan (EWT).

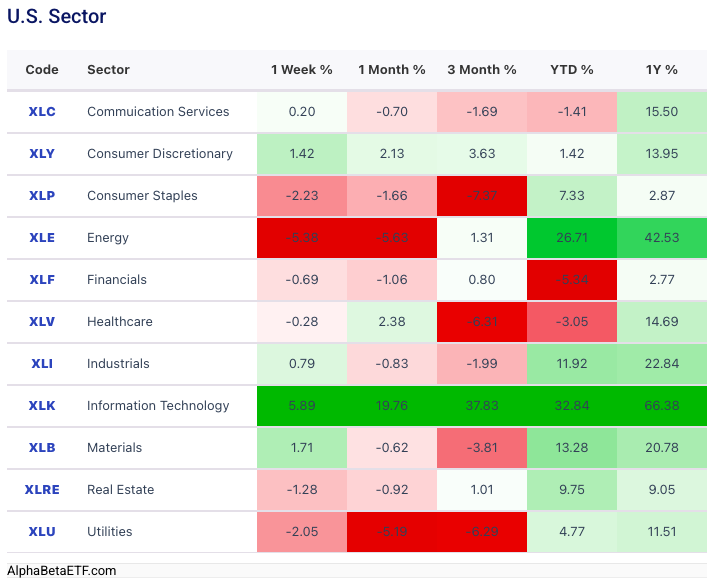

Tech sector continued to significantly outperform other sectors, while cyclical sectors including Consumer Discretionary, Non-Oil Energy, Industrials and Materials saw positive returns this week:

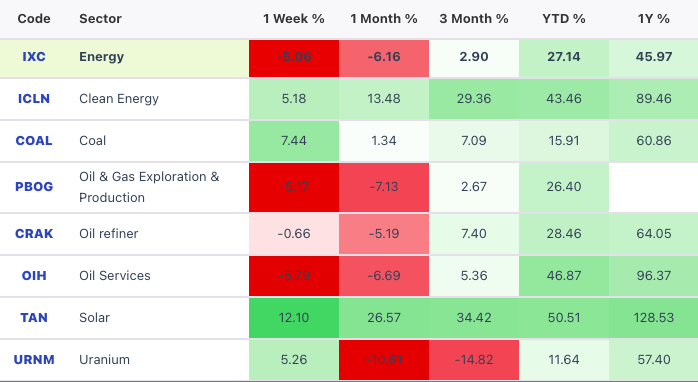

Despite the decline in oil price and thus oil companies, other non-oil energy companies saw material gains this week, captured by Clean Energy (ICLN), Coal (COAL), Solar (TAN), and Uranium (URNM):

Blue Origins’ New Glenn rocket exploded at the end of the week, sending space-related ETFs such as Procure Space ETF (UFO) and Tema Space Innovators ETF (NASA) down, and this happened only shortly before the IPO of SpaceX, although they still managed to capture around 3-5% gains during the week.

Within individual technology names, Micron surged after UBS raising its Micron price target to $1,625 with over 100% upside before the stock price spiked on the news. The bank argued that long-term agreements across the memory chip industry could fundamentally reshape Micron’s earnings profile and improve profitability visibility over multiple years. Dell’s AI server backlog and guidance drove the stock price by over 30% post earnings, as its AI server revenue exceeded its PC revenue. The company ended with an AI backlog over $50 billion, prompting a substantial uplift to full‑year profit and revenue guidance. These positive company news drove Memory and AI-related ETFs including Roundhill Memory ETF (DRAM), iShares A.I. Innovation and Tech Active ETF (BAI), and Global X Artificial Intelligence & Technology ETF (AIQ) to perform well.

Fixed Income

Treasuries rallied as softer consumer confidence, weaker growth, and easing oil fears pulled yields lower across the curve. Credit conditions showed some strain underneath the surface.

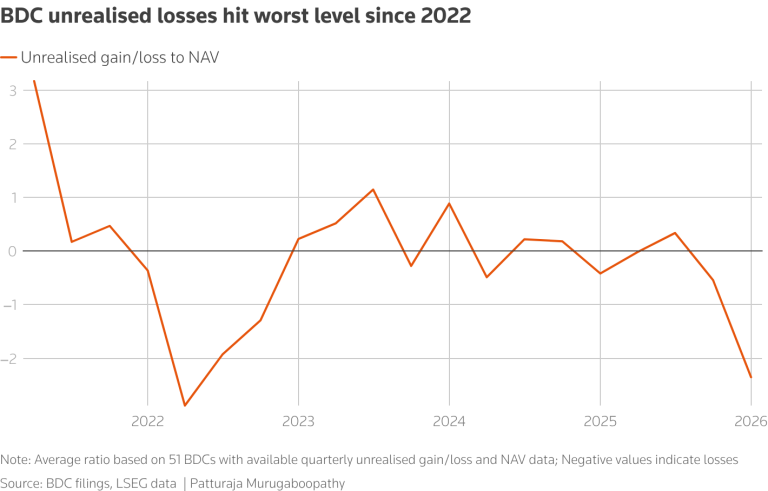

Unrealised losses at U.S. private‑credit lenders deepened in Q1 to their worst levels since 2022, with payment-in-kind (non‑cash interest) still elevated, an evidence that tighter financing conditions are gradually straining some borrowers.

Commodity

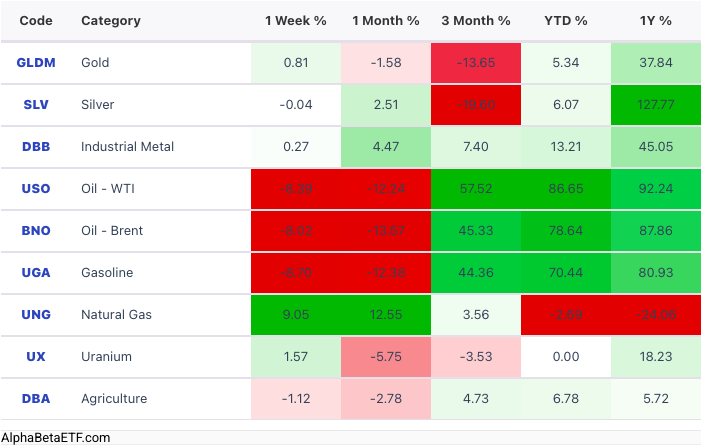

Oil (USO, BNO) dropped over 8% over the week as markets priced a credible U.S.–Iran deal and the possibility of a reopening of the Strait of Hormuz. However, the majority of other energy commodities such as Natural Gas (UNG) and Uranium (UX) rose during the week.

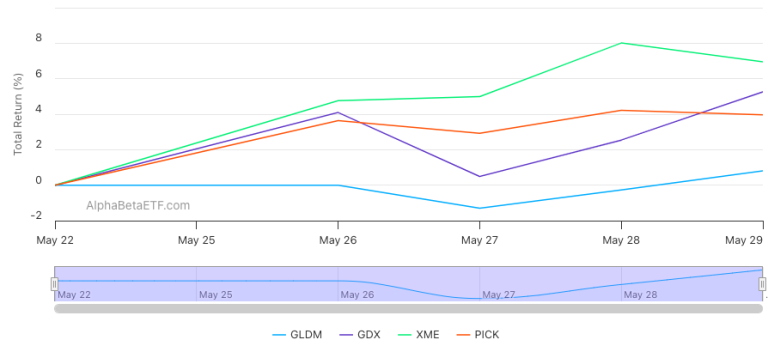

Gold (GLDM) moved more steadily, while Gold Miners (GDX) outperformed Gold by over 4% over the past week despite the modest gain in gold price. Metal miners (PICK) were also driven by Aluminium on news that Guinea, the globe’s largest bauxite producer, plans to introduce export restrictions on the mineral next month via new reforms to prop up prices. The country contributes more than a third of global bauxite output.

Currency

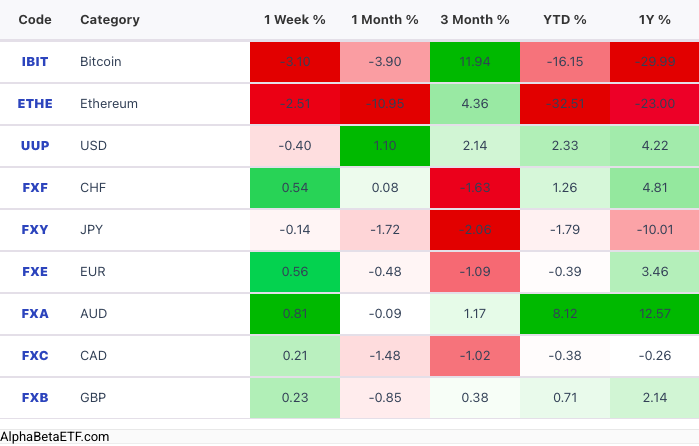

Bitcoin (IBIT) had a weak week and ended down around 3%, erasing the gains from the first half of the month and falling back below 74,000. The U.S. dollar was softer, while most major currencies gained modestly.

The yen (FXY) stayed under pressure near the 160 level, keeping intervention risk in focus. Tokyo’s core inflation (excluding fresh food) slowed to 1.3% year-on-year in May, marking the sixth consecutive month of deceleration and a four-year low. Headline inflation also eased to 1.4%. This cooling trend is largely driven by temporary government subsidies on utility bills and education fees. Service prices are still rising, and analysts expect inflation to re-accelerate in the coming months due to surging energy prices and import pressures from a weak yen, keeping expectations active for BOJ rate hikes.

The Week Ahead

US: May Nonfarm Payroll, Unemployment Rate

Europe: May CPI, April Unemployment Rate, Q1 GDP